By McKinsey’s David Feber, Oskar Lingqvist, Daniel Nordigården, and Matthew Seidner (originally published here and republished with permission)

The COVID-19 pandemic has forced consumer-goods companies to change priorities and pause new product launches within several categories. This has had a direct impact on the global packaging industry, as brand owners not only required fewer redesigns but also deprioritised innovative packaging. However, as the world begins to emerge from the current public-health and economic crisis, we anticipate that brand owners will accelerate their product-launch plans to address untapped market demand.

In parallel, the pandemic has also changed consumer behaviour, sparking new demands on packaging performance. To manage through the next normal, companies in the $900 billion-a-year global packaging industry will need to raise their game to be competitive. In this article, we highlight five strategic areas for packaging players to address as they prepare for a flood of new product launches.

First, seek out growth opportunities within the e-commerce sector by developing packaging formats tailored to this particular market. The pandemic has accelerated e-commerce adoption in several key segments (particularly grocery), and e-shopping is expected to be the consumer behaviour with the highest degree of post-pandemic “stickiness.”

Second, develop holistic solutions for sustainable packaging to address consumers’ increased demand for sustainable products: packaging companies need to go beyond the “must haves” (such as recyclability and recycled content) to integrate sustainability as a core element of their strategy.

Third, focus on future consumer needs and changing habits by creating a packaging experience that plays beyond mere convenience. Next, ensure that the company’s asset footprint has the flexibility to accommodate increased SKU proliferation and complexity: for example, consider both long-run, decidedly cost-efficient business and short-run, highly customised work.

Finally, embrace digital as a core component of the company’s strategic framework in areas ranging from customer interaction to enhancing manufacturing efficiency. We urge packaging companies to address these five imperatives as part of their strategy, while bearing in mind that a speedy, proactive approach is critical to creating value and capturing growth.

Catching the wave: Product launches post-COVID-19

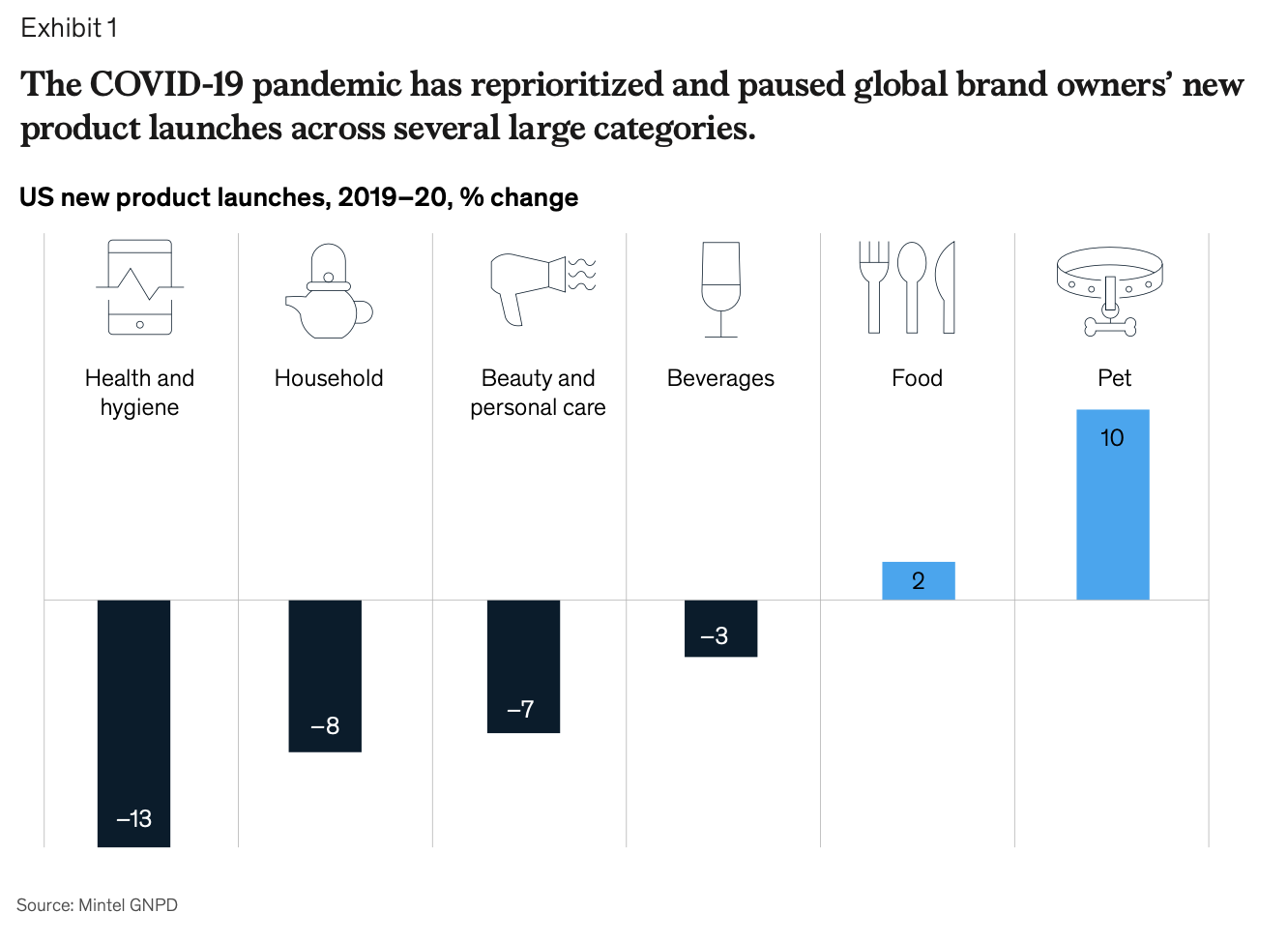

New product launches represent a key driver of both overall packaging demand and new packaging design and innovation. However, to some extent, the COVID-19 pandemic has caused global brands to pause new product launches in several categories (such as household products) and to switch priorities toward assuring product availability for consumers within categories such as food (Exhibit 1).

While new product introductions in the United States were down only some 3 percent in total during 2020 compared with 2019, on a more granular level several large categories experienced quite significant declines and priority shifts. For example, product introductions in health and hygiene showed an overall decline of some

13 percent as firms focused on supplying existing products to assure continuity for consumers.

Similarly, the large beauty and personal-care category saw a drop in new launches of around 7 percent as more people spending time at home dampened demand: both colour-cosmetics and fragrance lines saw an almost 20 percent decline in new launches; by contrast, new launches of soap products soared by around 50 percent, prompted by a heightened focus on hygiene during the pandemic.

While the food and pet-food segments experienced modest growth overall (approximately 2 percent and 10 percent, respectively), several subcategories saw strong change. For example, new product launches of chocolate confectionary and sugar and gum lines both declined more than 40 percent; however, other subcategories (such as soups, sauces and seasonings, sweet spreads, and fruits and vegetables) underwent a supercharged expansion in new product launches (up 30 to 50 percent), driven by work-from-home protocols and a growing health- and-wellness trend.

Now, as we begin to emerge from the pandemic, new product launches are expected to pick up once again. Spurred by increased consumer optimism, we expect to see the pace of new launches accelerating to catch up with the spend recovery. A similar pattern in the consumer-goods industry was seen following the Great Recession of 2008, when activity around innovation was muted before exploding in the years that followed.

That said, a lot has changed with COVID-19, and the resulting trends will shape both new product launches and packaging demand—in particular, consumer sentiment and behaviour have both shifted dramatically with the pandemic. More than 75 percent of Americans have tried a new shopping behaviour during the pandemic, with around 40 percent declaring that they have switched brands.

Value has been the main driver of consumers’ brand switching, although other reasons, such as purpose, quality, and novelty, have emerged. Gen Z and millennial consumers cite purpose and increasing preference for quality and organic products as key reasons to change brands. Another significant area is the accelerating popularity of online spending, which has seen a 35 percent year-on-year rise (from January 2020) in credit- and debit-card spend, sustaining the April 2020 jump in online spending caused by shelter-in- place rules.

Many of these new behaviors are expected to stick. In particular, the step change in digital adoption around e-grocery shopping and healthcare and wellness services is anticipated to remain at or near the elevated COVID-19 level.

Similarly, as a result of continued remote working, home nesting is expected to be an enduring lifestyle trend for many consumers who have invested in new uses for living spaces, such as home offices and fitness and entertainment facilities. As we emerge from the pandemic, leisure travel, in-person dining, and education are all due to resume, but we anticipate modifications to the consumer experience (such as contactless restaurant menus or virtual events).

At the same time, consumers are more concerned about sustainability than they were before the pandemic, and this will have a major impact on packaging choices going forward. Our recent survey found that more than half of US consumers are “highly concerned” about the environmental impact of packaging in general and report an increased willingness to pay for green packaging.

Five strategic areas for the packaging industry to address proactively

Many of the changes in consumer behaviour and demand will have critical ramifications for the packaging industry. As packaging companies ponder how they can be successful partners for the next wave of new product introductions, we see five strategic areas where they will need to be proactive (Exhibit 2).

1. Develop e-commerce-adapted packaging.

E-shopping is anticipated to be the most sticky consumer behaviour post-pandemic. Consequently, many current packaging formats will have to be updated or redesigned to optimise them for e-commerce and shipping: future packaging formats will need to prevent product damage, support productivity in the full supply chain, reduce transportation costs, and improve the consumer experience.

2. Rethink sustainability.

Packaging sustainability efforts are often centered around a desire to decrease leakage, improve circularity, and reduce carbon footprint. Going forward, we believe it will be important for packaging players to address sustainability as a core component of their strategic framework in three ways:

— Update and enhance the company’s product and technology-strategy road map with relevant sustainability narratives.

— Identify growth opportunities, potential lighthouse projects, and the partners needed to deliver them.

— In cases where no solution can be developed, understand the areas of risk if volumes move to alternative substrates.

As a starting point, we suggest creating an actionable fact base, at a granular and local level, to understand evolving consumer sentiments, as well as brand owner and retailer preferences and developments, in relation to sustainability.

3. Cater to changing consumer needs and habits. Lasting behavioural shifts have already resulted from the pandemic. To support brand owners with their product launches, packaging companies need to respond to such changing behaviours, for example, by developing packaging that can help to address Gen Z and millennials’ preferences for purpose, quality, and novelty.

4. Develop a flexible asset footprint. Changes to the value chain in response to e-commerce and consumer shifts will increase SKU complexity. We are likely to see continued demand for long- run, cost-efficient packaging formats, as well as acceleration for fully customised short-run packaging. This polarisation in packaging formats will mean that companies need to improve their flexibility and capacity to accommodate different packaging production requirements.

5. Embrace digital end to end. The packaging industry is in the early stages of adopting digital. This offers significant potential with respect to both reducing costs and increasing revenue and working capital. In a recent survey, half of those responding saw potential for companies to achieve a revenue and working-capital boost of more than 5 percent, while about 70 percent suggested digital adoption could lead to overall cost improvements of more than 5 percent. Digital also offers major opportunities for both increased customer interaction and tracking and tracing. With the right approach and execution focus, packaging companies should be able to pursue the sizable cost-efficiency, growth, and productivity opportunities offered by digital.

Packaging companies have the opportunity to create value and capture growth as brand owners revamp their product launches in the next normal. Success will require an innovation mindset combined with the right strategic choices in the context of evolving megatrends. A proactive approach will help companies stay on top of market developments, while simultaneously creating an opportunity to become a thought partner for customers.

David Feber and Daniel Nordigården are partners in McKinsey’s Detroit office, Oskar Lingqvist is a senior partner in the Stockholm office, and Matthew Seidner is a senior advisor in the Chicago office.

The authors wish to thank Maimouna Diakhaby, Maximilian Fischer, Abhinav Goel, Anne Grimmelt, and Emily Roeper for their contributions to this article.